Introduction

Even as payment enterprises deal with higher asset values, confront stronger opponents, and heightened predispose variables exacerbated by pandemic, they are being pushed quickly towards change.

Payment volumes reached record highs before the epidemic, and are set to witness strong growth, although at a slower rate, indicating both the increased dependence on non-cash transactions & the impact of a sluggish international market.

According to the study

- Global non-cash transactions climbed by 12.78% from 2021 to 2022, reaching 946.8 billion money transfers.

- Global non-cash transactions will rise at a compound annual growth rate of 9.22% from 2021 to 2023.

- With 318.9 billion in non-cash transactions, Asia-Pacific has eclipsed Europe and North America to take the lead in 2021 and is estimated to have 390.8 billion transactions in 2021.

- Smart mobile penetration, rising e-com, digital wallet use, and mobile/QR-code payment revolutions, spearheaded by China, India, and other SE Asian economies, drove the surge (31.1 percent growth).

Traditional payment providers are being pushed to innovate as a result of increased competition.

As customers' demand for digital payments increases, companies are shifting away from cash. New entrants are quickly gaining in popularity, as per the survey conducted by Capgemini.

- For payment services, 30% of users prefer Biotech giants like Facebook, Amazon, Facebook, Apple, Alibaba, and many others.

- 50% have been using a challenger bank service (Recently established banks with its operating system that work in conjunction with major financial institutions, often by concentrating in locations where the larger banks are not present are identified as a challenger bank. Examples are NuBank, Chime, and Monzo) for several payments. Indian examples of challenger banks are Airtel Payments Bank, Jio Payments Bank, 811, Paytm Payments Bank, and InstantPay.

- Over 38% of individuals claimed they found the perfect method of payment during the pandemic.

- E-banking and direct account transfers have been and continue to be the favored payment method during the worldwide health catastrophe, as per 68 percent of customers.

- Contactless (tap-to-pay) cards ranked second for the favourite way of payment, with 64 percent saying they use them frequently.

- Digital wallets (including QR-based payments) were considered as the most suitable method of the transaction by 48 percent of those surveyed.

- Alternative transaction services likely attract a lot of attention as consumers seek efficiency, pace, and a positive customer service.

- By 2024, the group of individuals using digital wallets is predicted to increase from 2.98 billion in 2021 to 4 billion, accounting for half of the world's population.

- Transparent transactions, or automated payment mechanisms, are expected to rise at a 51 percent CAGR in 2022.

Payments providers can overcome increased risks with the use of technology and teamwork.

- As the economy expects to be affected and more forms of payment become available, payment providers must deal with rising threats in their company, regulations, and administration. Payments executives say organizations are exposed to risks such as cyber safety (42%), legislative (37%), logistics (35%), and business (30%).

- As cybercriminals are leveraging the COVID-19 lockout's exposed weaknesses, which raises the risk of hacks, financial fraud, and global terrorism, 87% of CEOs believe they have a high risk of cyber threats. Payments providers are aggressively utilizing technology to assist mitigate the risk of emerging dangers.

- Corporate treasurers today want better API connectivity, risk assessment, and real-time transactions and monitoring from their banks and payment providers.

- Payments transformation looks to be unavoidable as digitalization (75%) & client-visible innovation (79%) are the main factors of bank CEOs' strategic ambitions for 2020 beyond.

- The partnership is the core of the shift & it can help with epidemic uncertainty, particularly with non-cash payments, as policymakers emphasize preventive measures.

- Developing in-house talents or working with digitized innovative new startups are two methods financial institutions (banks) are considering to create a smaller, more flexible backend that can balance with a digital front-end.

- 60 percent of the executives of financial institutions (banks) feel that cooperating with 3rd party companies throughout the production process will help them strengthen enterprise services in addition to strengthening in-house abilities.

Appraisal of the Impact of Application Leaders in Charge of Digital Commerce Payments

Impact and Suggestions

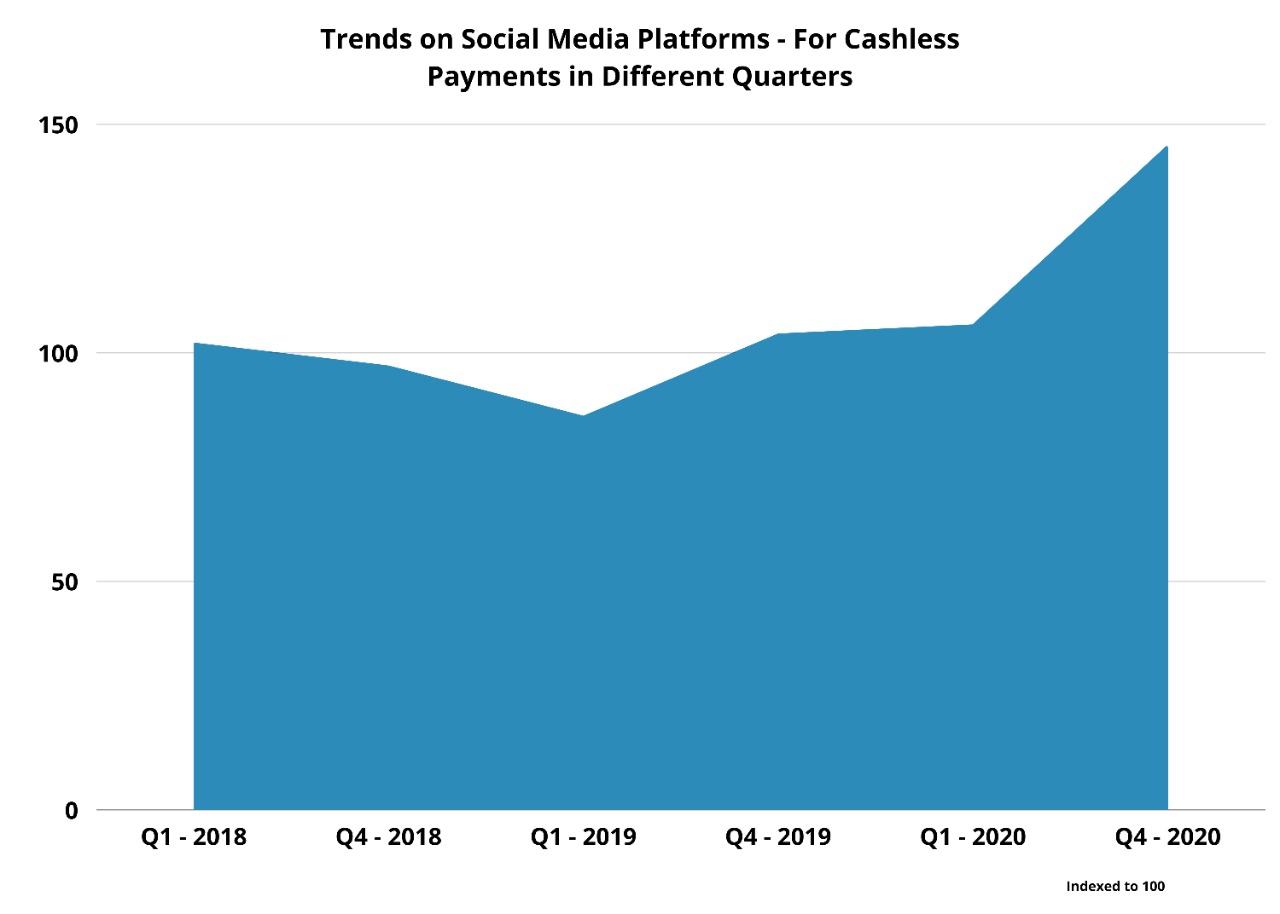

Nevertheless, whether or not the COVID-19 virus spreads in this way, cash and PIN pads do carry germs, and being customer-centric when reopening to the public includes being aware of your customers' and employees' perceptions of money handling. As per a Gartner data analysis, conversations on contactless payments surged approximately 40% in the second quarter of 2020, indicating that COVID-19 has had a significant influence on the rise in popularity of contactless payments on social media.

Both for its quick, safe, and touchless interface, contactless technology emerged as the new payment technology. Over 100 markets witnessed contactless as a portion of total in-person payments that climbed by at least 50% between the 1st quarter of 2020 and the 1st quarter of 2021. The first quarter of 2021 observed 1 billion more contactless transactions than in the same period of 2020. In emerging markets, contactless technology rose by 1x to 2x year-over-year.

Pandemic Effects - Contactless Payment

Buy Now Pay Later (BNPL) payment methods may be a possible payment winner as a result of the epidemic. COVID-19 has ramifications for the global economy as well. Alternative financing methods grow more enticing when customers' incomes grow more limited and cash-strapped. Consumers can take advantage of BNPL's installment and deferred payment options, which are normally given at 0% interest. This, paired with the digital revolution, is leading to widespread use of BNPL payment methods, even in countries that are trailing behind, such as the United States of America.

Service providers like Estel Technologies provide adaptability

There are a wide range of e-payment technology solutions provided by Estel, designed to reduce transaction time, expenses and operational complexity while increasing customer satisfaction & retention. These solutions ease the transactions as per the situation and customers’ requirements.

Estel's m-POS Solution is a one-of-a-kind, low-cost & flexible mobility solution that enables smartphones to be used as Mobile POS (mPOS) systems, with the same functionality as standard POS systems for accepting and processing card-based payments. It allows vendors and businesses to provide their card-based clients a dedicated network of service. Through a digital interface, the solution provides contactless technology with professional and technical services as per the market’s demand.

The Estel Merchant Payment Aggregator solution streamlines the payment process for businesses by allowing them to accept multiple types of digital cashless payments from several sources using a smartphone. This allows Payment Service Providers (PSPs) to attract merchants by providing them the Estel solution, which combines all digital payment methods in a single app with single-window merchant administration and a single point settlement.

With Estel Mobile Wallet, unbanked customers can now access financial services by enabling opening of virtual accounts at local agents, and enabling cashless transfers & payments to merchants for goods or services. The solution also enables end customers to receive inward international remittances seamlessly & directly into their mobile wallets or bank accounts.

With Estel's unique card-less Agency Banking system, provides facility of branchless banking, increased reach and accessibility while lowering capital expenditure costs significantly for banks. Branchless banking use in emerging economies, amidst the pandemic is predicted to be revolutionized by this innovation.

The Estel MMO Switch provides a complete set of solutions for Interoperability between various mobile money services, as well as between these mobile money services and the traditional financial institutions (banks), to further drive up usage of these services.

Estel Technologies products have high capability to meet the rising enthusiasm for the future state of payment methods.

References:

- Gartner: Payment Acceptance Will Never Be the Same After the COVID-19 Pandemic

- World Payments Report 2020

- Mapping Mobile Wallet Payments 2021 Around the World by Expert Market

- Mastercard New Payments Index 2021: Consumer Appetite for Digital Payments Takes Off

Written By: Jenie Singh (Marketing Exec - Estel Technologies) A homo sapiens, Alumni of BIT Mesra & NIT Durgapur and a Marketing Enthusiast with Bachelors in Architecture and Masters in Business Administration with a specialization in Marketing.

You may also like